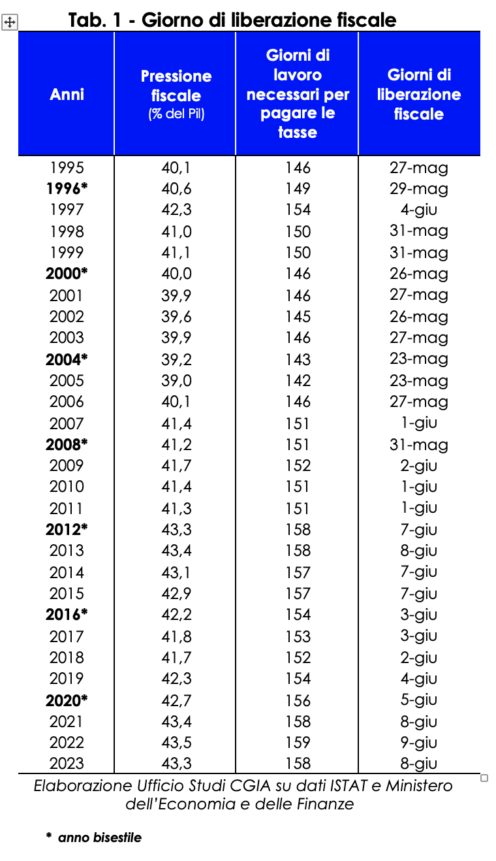

This we are about to conclude is the last weekend of the year that we work for the taxman. In purely theoretical terms, in fact, next Wednesday Italian taxpayers1 will finish paying the taxes, levies and social contributions necessary to run schools, hospitals, transport, to pay salaries to public employees, pensions, etc. Thursday 8 June, therefore, we celebrate the "day of tax release"; in other words, if from the beginning of January to 7 June we worked to honor the demands of the tax authorities, from the following day until next 31 December, however, we will do it for ourselves and for our families. From this school case developed by the CGIA Research Office, it emerges that for the current year 158 working days were needed (Saturdays and Sundays included) to fulfill all the tax payments foreseen this year (Irpef , Imu, Iva, Irap, Ires, various surtaxes, social security/insurance contributions, etc.). Compared to 2022, this year's tax freedom day "falls" one day earlier.

The calculation methodology

How did it come to be established that June 8 is the "tax liberation day" of 2023? The estimated national GDP expected this year (2.018.045 million euros) was divided into 365 days, thus obtaining an average daily figure (5.528,9 million euros). Subsequently, the revenue forecasts from taxes, duties and social security contributions2 that income recipients will pay this year (874.132 million euros)3 were "recovered" and compared to the daily GDP. The result of this operation allowed the CGIA Research Office to calculate the 2023 tax freedom day 158 days after the beginning of the year, i.e. next 8 June.

In 2022 historical record of the tax burden

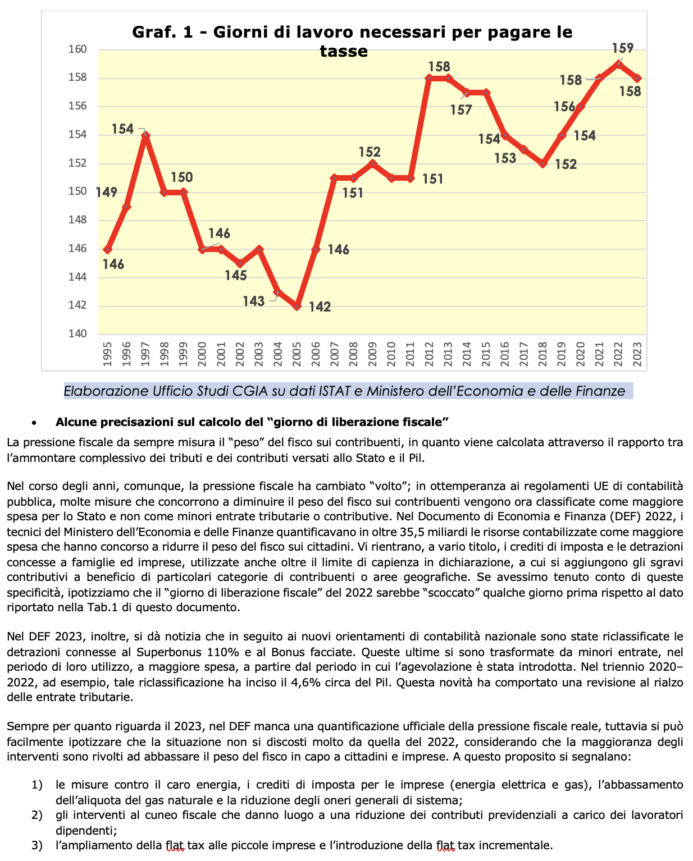

Since 1995, the date of the "tax liberation day" furthest in the calendar has occurred in 2005. On that occasion, the tax burden stood at 39 per cent and Italian taxpayers was "enough" to reach May 23 (142 working days) to leave behind the economic commitment required by the tax authorities. Still observing the calendar, the most "delayed" one, however, was recorded in 2022, when the tax burden reached the all-time record of 43,5 percent and, consequently, the "tax liberation day" ” on June 9. It is correct to point out that the record peak in the tax burden reached last year is not attributable to an increase in the levy imposed on households and businesses, but to a series of other factors that were concentrated in 2022. In particular: from the surge the cost of imported energy products and the marked increase in inflation which pushed up the revenue from VAT; by the increase in employment which contributed to an increase in direct taxes and social security contributions. At the same time - in compliance with the European dictates relating to public accounting - the resources to finance building bonuses and tax credits, the latter introduced to mitigate high bills, were classified as higher public expenditure and not as lower revenue.

In the EU, only France and Belgium pay more than us

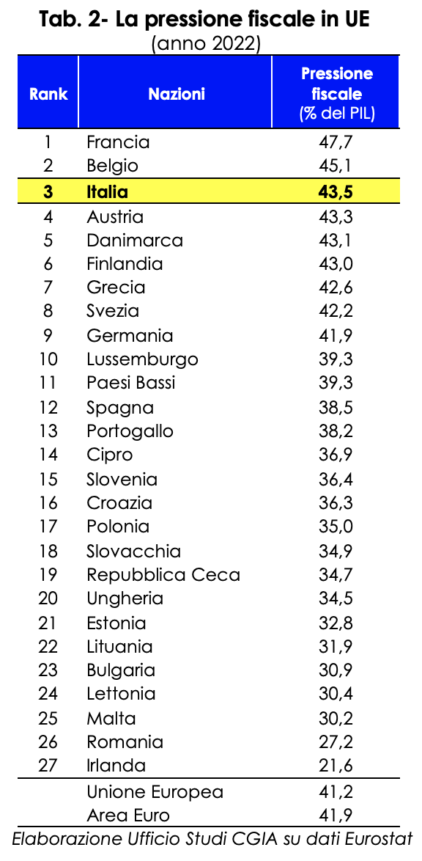

The "tax liberation day" is not an absolute principle, but a theoretical exercise that demonstrates empirically, if there were still any need, how excessive the tax burden weighing on Italians is. A specificity that emerges to an equally evident extent when we compare our tax burden with that of EU countries. In 2022, in fact, only France and Belgium recorded a higher tax burden than ours. If in Paris the tax burden was 47,7 percent of GDP, in Brussels it stood at 45,1 percent. Here, on the other hand, it reached the record threshold of 43,5 percent. Among the 27 in the EU, Italy "placed" in third place. Germany, on the other hand, ranked 9th with a tax burden of 41,9 per cent, while Spain is in 12th place with 38,5 per cent. The average of the countries of the Euro Area was 41,9 per cent.

June's tax bottleneck: 115 deadlines, on average 4 per day

If the CGIA study represents a real school case, the reality, unfortunately, still has very high levels of complication/difficulty. In this month of June, for example, Italian taxpayers are "expected" by as many as 115 tax "appointments", on average almost 4 a day. The calendar includes:

- 50 deadlines (substitute tax, VAT, withholding taxes, Tobin tax, entertainment tax, etc.), by 16 June;

- 1 communication of the TV fee by 20 June;

- 55 payments (IRPEF, surtaxes, dry coupon, withholdings, VAT, IRES, IRAP, substitute taxes, etc.), 4 declarations (IRPEF, substitute taxes, intra, etc.), 4 communications (lease agreements, financial information for tax purposes between EU states, etc.) and a TV license application by 30 June.

These deadlines, obviously, will not affect all taxpayers, however they give a sense of the cumbersomeness and complexity of our tax authorities.

Wealthier regions pay more taxes

It is the citizens of the Autonomous Province of Bolzano who pay the highest number of taxes to the tax authorities. In 20194, each resident of this area paid an average of 13.158 euros in taxes, duties and levies. Followed by the Lombards with 12.579 euros, the Aosta Valley with 12.033 euros, the Emilia-Romagna with 11.537 and Lazio with 11.231 euros. Calabria, on the other hand, is the area where the "burden" of the tax authorities is lower: each resident of this area paid an average of 5.892 euros to the treasury. The national average is equal to 9.581 euros.

The strong gap between the north and south of the country shouldn't surprise us. Our tax system, in fact, is based on the criterion of progressiveness. Therefore, in regions where income levels are higher, thanks to better economic and social conditions, tax revenues are also higher than elsewhere. It should also be noted that in geographical areas where the primary sector has a significant impact on the overall economy, the benefits provided by the legislator (in particular tax deductions) significantly reduce the tax base of taxpayers belonging to these activities and, consequently, also the total revenue from taxes paid to the Treasury by that region. Finally, for the calculation of regional per capita revenue, the total amount of taxes paid to the tax authorities by each territory was considered, therefore the figure will be higher especially in the geographical realities where the presence of economic activities is more widespread.

Some clarifications on the calculation of the "tax release day"

The tax burden has always measured the "burden" of the taxman on taxpayers, as it is calculated through the ratio between the total amount of taxes and contributions paid to the State and the GDP.

Over the years, however, the tax burden has changed "face"; in compliance with EU public accounting regulations, many measures that contribute to reducing the tax burden on taxpayers are now classified as higher expenditure for the State and not as lower tax or social security revenues. In the Economic and Finance Document (DEF) 2022, the technicians of the Ministry of Economy and Finance quantified the resources accounted for as the greatest expense at over 35,5 billion, which contributed to reducing the tax burden on citizens. This includes, for various reasons, tax credits and deductions granted to households and businesses, also used beyond the capacity limit in the declaration, to which are added the tax relief for the benefit of particular categories of taxpayers or geographical areas. If we had taken these specificities into account, we assume that the 2022 "tax release day" would have "occurred" a few days earlier than the data reported in Table 1 of this document.

Furthermore, in the DEF 2023, it is reported that following the new national accounting guidelines, the deductions connected to the Superbonus 110% and the Bonus facades have been reclassified. The latter have been transformed from lower income, in the period of their use, to greater expenditure, starting from the period in which the subsidy was introduced. In the three-year period 2020-2022, for example, this reclassification affected around 4,6% of GDP. This novelty has led to an upward revision of tax revenues. Still with regard to 2023, the DEF lacks an official quantification of the real tax burden, however it can easily be assumed that the situation does not differ much from that of 2022, considering that the majority of interventions are aimed at lowering the tax burden in for citizens and businesses. In this regard, the following should be noted:

- measures against high energy costs, tax credits for businesses (electricity and gas), the lowering of the natural gas rate and the reduction of general system costs;

- interventions on the tax wedge which give rise to a reduction in the social security contributions payable by employees;

- the extension of the flat tax to small businesses and the introduction of the incremental flat tax.