In Milan (35.342 €), Monza-Brianza (31.984 €) and Bolzano (31.483 €) the realities most in the "red". The least ones are Agrigento (€10.302), Vibo Valentia (€9.993) and Enna (€9.631).

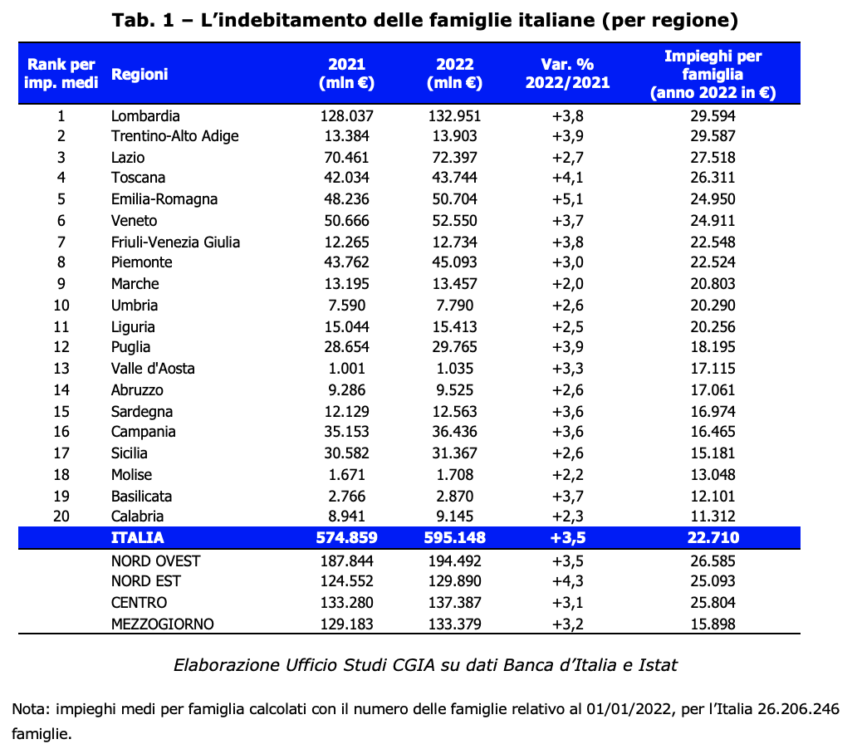

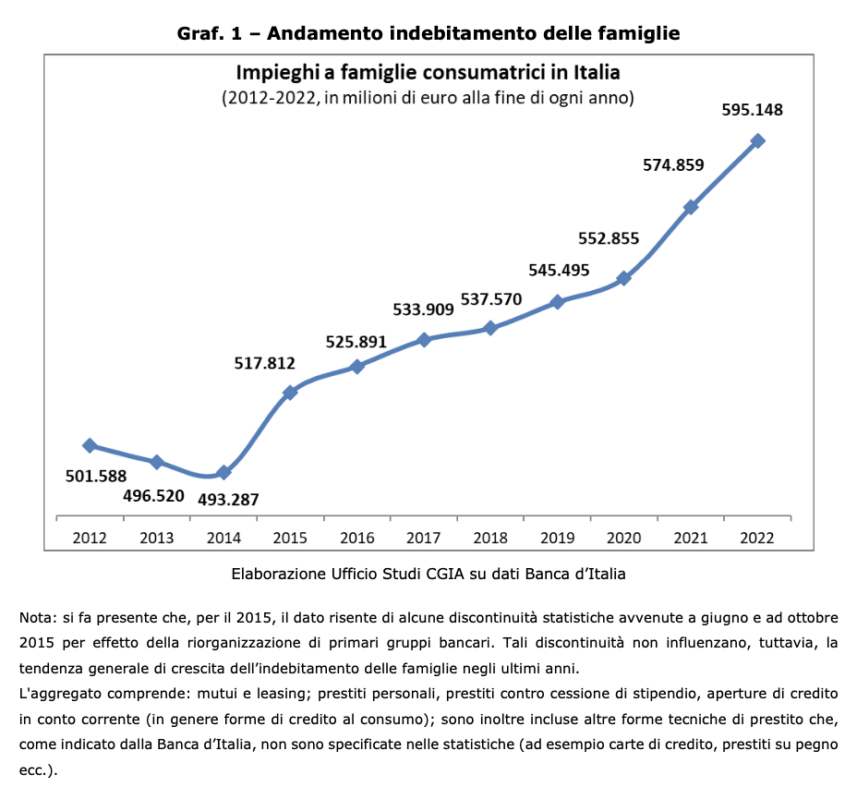

As at 31 December 2022, the average amount of debt per household in Italy had risen to 22.710 euros. Overall, the stock of bank debt held by all Italian households stood at a record level of 595,1 billion euros and increased by 3,5 percent compared to 2021.

To account for it is the CGIA Research Office which, following these results, fears another risk: the resurgence of usury. Although the number of reports of this crime to the police forces has been declining for some time, it cannot be excluded that the increase in household debts is driving more than one person to turn to usurers who have always been more "available" than anyone else to help those who are cash-strapped, especially in the most economically difficult times. Everyone knows that usury is a "karstic" phenomenon: those who have fallen into the network of loan sharks hardly turn to the police. Victims are very often threatened and are afraid for their physical safety and that of their loved ones. In fact, those who want their money back have no scruples; not only does he apply appalling interest rates within a few months, but he is willing to do anything to recover what has been lent, even in the last resort in the harshest ways.

• Critical situation, but still under control

Although the stock of debts is increasing due to inflation, the increase in the cost of mortgages and the surge in bills which negatively impacted much of last year, the situation is critical, but still under control. It is probable that the increase in debts is partly attributable to the strong economic recovery that took place in the two-year period 2021-2022. In fact, the most economically exposed provincial areas are also those with the highest income levels. Surely in these realities among the indebted there are also nuclei belonging to the weakest social groups. However, the higher indebtedness of these territories could be attributable to the significant investments made in recent years in the real estate sector which, obviously, are mostly attributable to families who have a good standard of living. Another thing, however, is to interpret the data from the South; in absolute terms the situation is less critical than in the rest of the country, even if the debt burden of the poorest households is certainly greater than elsewhere. It should also be remembered that the greatest incidence of debt on income is recorded in the most economically vulnerable households, i.e. in those at risk of poverty and social exclusion. Furthermore, Istat data tell us that the crises that have occurred since 2008 have increased the number of households in economic difficulty, given that the effects of these economic shocks have widened the gap between poor and rich.

• ARTISANS, RETAILERS AND VAT NUMBER THE MOST EXPOSED TO THE RISK OF USURY

With the progressive slowdown of the economy and the consequent collapse of bank loans to businesses in recent months, it cannot be excluded that there is an "approach" of criminal organizations towards family-run micro-companies: such as artisans, shopkeepers and many VAT numbers. The world of self-employed workers has always been the most at risk. In the past, following an unforeseen expense or a lack of collection, many were forced to go into debt for a few thousand euros with subjects who initially presented themselves as benefactors, but within a few months they transformed into what they really are: of criminals. To avoid all this, the trend must be reversed, returning to giving liquidity to micro-enterprises, otherwise many of these could end up in the arms of usurers. Not only that, it is also necessary to encourage recourse to the "Fund for the prevention" of usury. An instrument, the latter, introduced by law a few decades ago, but little used, also because it is unknown to most people and, consequently, with scarce economic resources available.

• THE FAMILIES MOST IN "RED" IN MILAN. IN ENNA THOSE LESS

The families most in the "red" are located in the province of Milan, with an average debt of 35.342 euros (+5,1 percent compared to 2021); in second place we see those of Monza-Brianza, with 31.984 euros (+3 percent) and in third place the residents of Bolzano, with 31.483 euros (+5 percent). Just off the podium we note those of Rome, with an average debt amounting to 30.851 euros (+2,8 percent) and those of Como, with 30.276 euros (+3,8 percent). Among the least exposed, however, we point out the families residing in the province of Agrigento, with a debt of 10.302 euros (+3 percent) and those of Vibo Valentia, with 9.993 euros (+1,9 percent). Finally, the least indebted households in Italy are found in Enna, with a "red" of 9.631 euros (+3,6 percent). In 2022, the Italian province that experienced the most significant growth variation in household debt was Ravenna (+9,1 per cent), while the only one that suffered a contraction was Vercelli (-2,3 per cent). hundred).